Diese Cookies und andere Informationen sind für die Funktion unserer Services unbedingt erforderlich. Sie garantieren, dass unser Service sicher und so wie von Ihnen gewünscht funktioniert. Daher kann man sie nicht deaktivieren.

Zur Cookierichtlinie

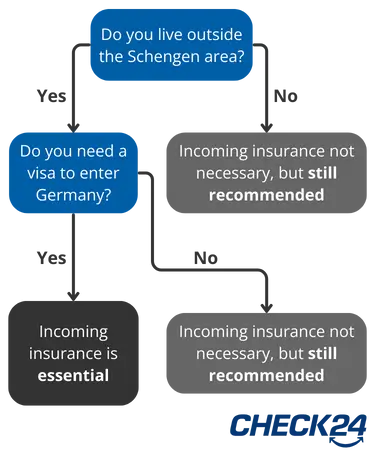

Incoming insurance is a special type of travel insurance. It is aimed almost exclusively at foreign guests who have to apply for a visa to enter the Schengen area. It can also be taken out by residents of the Schengen area who wish to extend the insurance cover of their home country during their trip.

The insurance can be purchased by both the foreign guest and the domestic host. In contrast to other travel insurance policies, incoming insurance is not available as annual cover, but only for the duration of the trip. Long-term incoming insurance can insure the guest for up to 60 months.

As a rule, incoming insurance must be taken out before the start of the trip. In this case, insurance cover begins from the moment you cross the border and ends after the agreed term. Some providers allow you to take out a policy up to two days after entering the destination country.